Reasons for the Decline in Housing Prices in Toronto: An Analysis of Affordability from 2000 to 2025

Toronto’s housing market has long been a symbol of Canada’s economic vitality, but in recent years, it has experienced a notable downturn. Detached home prices, which surged dramatically over the past two decades, began declining around 2022 and continued into 2025. This shift comes amid broader economic pressures, including stagnant wage growth relative to housing costs. By comparing average detached house prices and average salaries from 2000 to 2025, this article explores how affordability challenges have contributed to the market correction, alongside other key factors such as interest rates, inventory levels, immigration trends, and economic uncertainty.

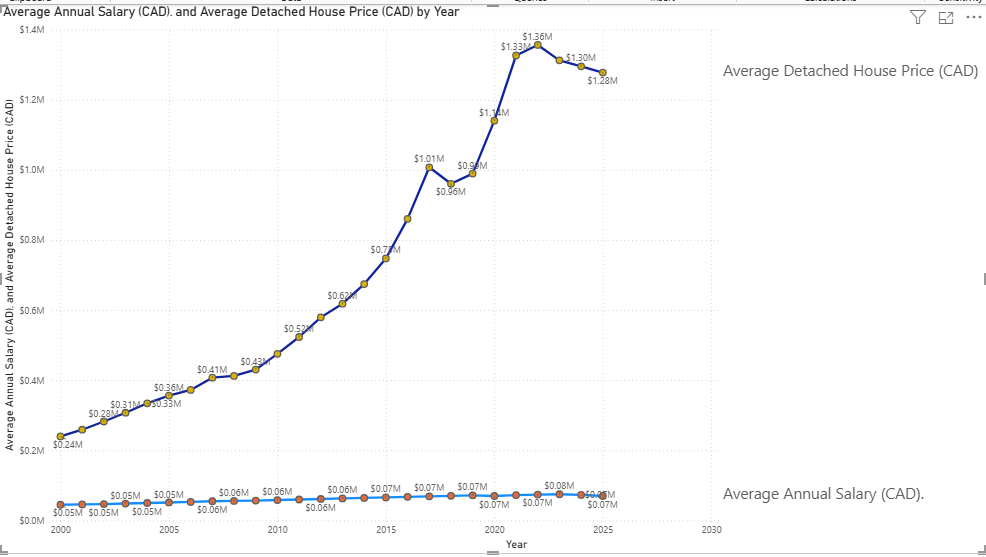

Historical Trends in Detached House Prices

Toronto’s detached housing market saw explosive growth from the early 2000s, driven by low interest rates, population influx, and investor demand. However, prices peaked in 2022 before entering a decline phase. The following table summarizes yearly average detached house prices in Toronto, based on market data.

From 2000 to 2022, prices increased by over 460%, far outpacing inflation and wage growth. The decline since 2022—approximately 6% by mid-2025—marks a significant reversal, with year-over-year drops in detached home values reported as high as 4.5% in some months.

Historical Trends in Average Salaries

In contrast to housing prices, average salaries in Toronto have grown more modestly. Data on employment income shows steady but slower increases, influenced by economic cycles, including the 2008 financial crisis and the COVID-19 pandemic. The table below provides approximate yearly average employment incomes, drawn from statistical sources and adjusted for overall trends (averaging men and women where gender-specific data is available). Recent figures for 2023-2025 are based on market reports, with averages around $60,000-$70,000.

Salaries rose by about 55% from 2000 to 2022, with recent stagnation due to inflation and job market shifts. This growth pales in comparison to housing appreciation, highlighting a growing affordability gap.

Comparative Analysis: The Affordability Crisis

A key metric for understanding the market decline is the house price-to-salary ratio, which measures how many years of average salary are needed to buy a detached home (assuming no other costs). In 2000, the ratio was around 5.3 (house price ~$240,000 / salary ~$45,000). By 2022, it ballooned to 18.3 ($1,356,479 / ~$74,000), making homeownership increasingly unattainable for average earners.

This erosion of affordability has directly contributed to reduced demand, as potential buyers—particularly first-time ones—are priced out. As ratios exceeded sustainable levels (typically 3-5 for healthy markets), the market corrected, with prices falling to align more closely with incomes. By mid-2025, the ratio dropped to about 18.3 ($1,277,667 / ~$70,000), but remains historically high, signaling ongoing pressure.

Key Reasons for the Decline

The mismatch between wages and housing costs is foundational, but several interconnected factors have accelerated the downturn since 2023:

- Rising Interest Rates and Mortgage Costs: The Bank of Canada’s rate hikes from 2022 to 2024 increased borrowing costs, reducing buyer purchasing power. Even as rates began easing in 2025, the lingering effects suppressed demand, leading to price drops of 2-5% annually.

- Surge in Inventory and Supply: Toronto saw “decades-high” listings in 2025, with new inventory up 35% year-over-year in some periods. This oversupply, combined with fewer sales, forced sellers to lower prices. Construction slowdowns for new homes exacerbated the issue, as weak demand deterred builders.

- Slower Population Growth and Immigration: Canada’s reduced immigration targets in 2024-2025 curbed population influx to Toronto, a key driver of past demand. With fewer newcomers, buyer pools shrank, contributing to a 5.2% year-over-year price decline in some segments.

- Economic Uncertainty and Job Market Weakness: High inflation, trade tensions, and a softening economy have made buyers cautious. Unemployment in Toronto hovered around 8-9% in 2025, and stagnant salary growth amid rising living costs further eroded confidence.

- Policy and Market Corrections: Past policies like the 2017 Fair Housing Plan initially cooled the market, and ongoing affordability initiatives (e.g., mortgage stress tests) have sustained downward pressure. Pre-construction condo challenges also spilled over to detached homes.

Outlook and Implications

While the decline offers some relief for buyers, it poses risks for homeowners and the economy, including potential negative equity for recent purchasers. Forecasts suggest prices may stabilize or rise modestly by 2026 if interest rates continue falling and economic conditions improve, but without wage growth catching up, affordability will remain a barrier. Toronto’s market serves as a cautionary tale: unchecked price growth detached from incomes inevitably leads to corrections. Policymakers must prioritize supply increases, wage support, and targeted incentives to foster a balanced recovery.